Attention: Please take a moment to consider our terms and conditions before posting.

Savings and Investments thread

Comments

-

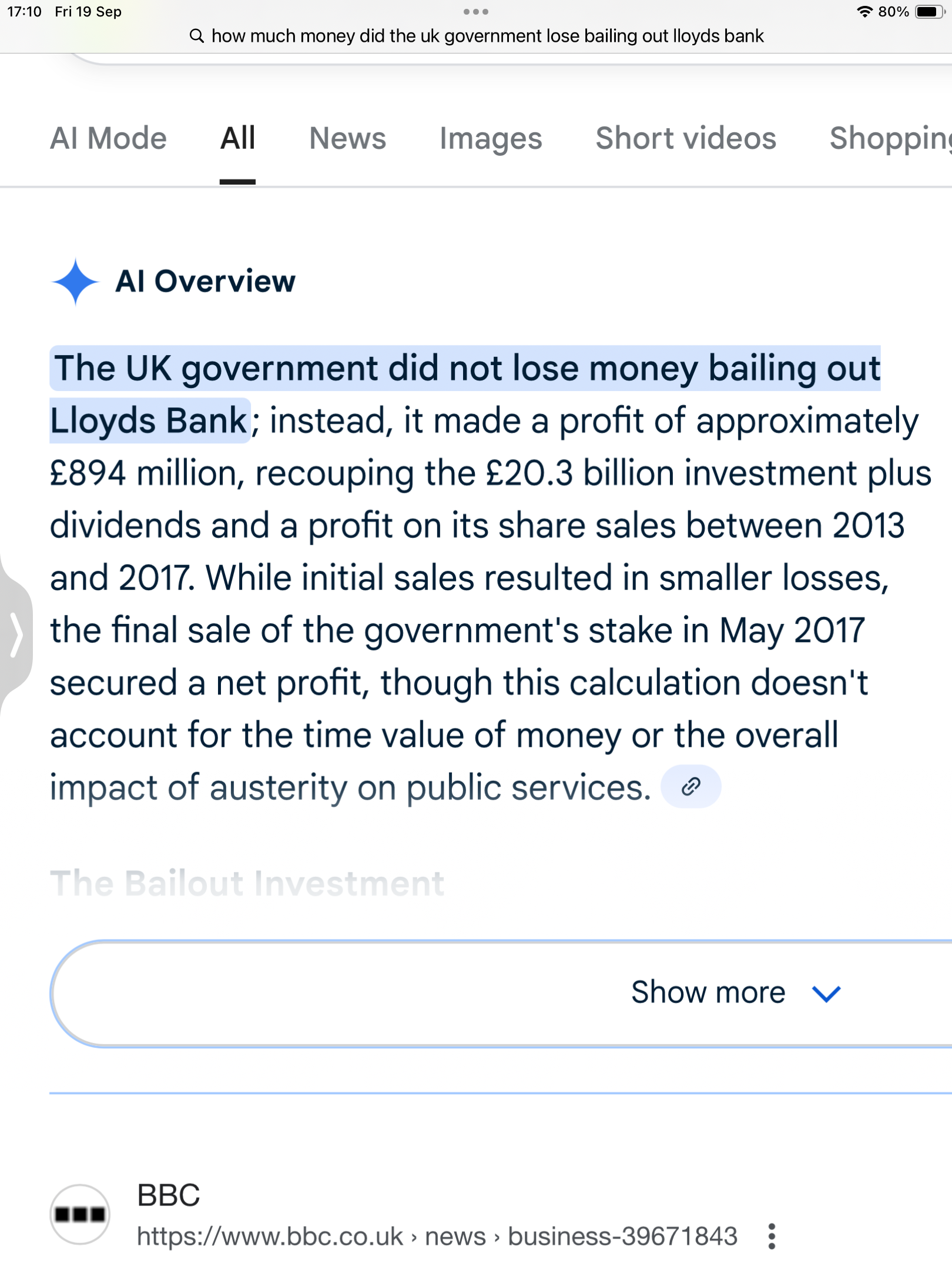

I just like the true facts of this case to be seen. Many people believe their Tax money saved Lloyds Bank. That is completely untrue. The facts are that Lloyds Bank shareholders saved the UK Government from an unprecedented run on the banking sector not seen since the 1920,s.

1

1 -

I stand corrected, although as that piece says, what did the taxpayer lose in the interim with austerity & the money could have been used elsewhere.RaplhMilne said:I just like the true facts of this case to be seen. Many people believe their Tax money saved Lloyds Bank. That is completely untrue. The facts are that Lloyds Bank shareholders saved the UK Government from an unprecedented run on the banking sector not seen since the 1920,s.

I'm of the firm belief that shareholders should never be bailed out. You buy shares in the knowledge of the risk involved. Different for depositors, although as I said yesterday, I believe the FSCS is too generous.0 -

And if all the retail account holders lost their savings there would have been additional issues.golfaddick said:

I stand corrected, although as that piece says, what did the taxpayer lose in the interim with austerity & the money could have been used elsewhere.RaplhMilne said:I just like the true facts of this case to be seen. Many people believe their Tax money saved Lloyds Bank. That is completely untrue. The facts are that Lloyds Bank shareholders saved the UK Government from an unprecedented run on the banking sector not seen since the 1920,s.

I'm of the firm belief that shareholders should never be bailed out. You buy shares in the knowledge of the risk involved. Different for depositors, although as I said yesterday, I believe the FSCS is too generous.It was a unique global crisis that really had few options as to best address.1 -

Bang on. Now let's apply that to the water companies. I'm sorry, Canadian teachers, but screw your stupid pension fund trusteesgolfaddick said:

I stand corrected, although as that piece says, what did the taxpayer lose in the interim with austerity & the money could have been used elsewhere.RaplhMilne said:I just like the true facts of this case to be seen. Many people believe their Tax money saved Lloyds Bank. That is completely untrue. The facts are that Lloyds Bank shareholders saved the UK Government from an unprecedented run on the banking sector not seen since the 1920,s.

I'm of the firm belief that shareholders should never be bailed out. You buy shares in the knowledge of the risk involved. Different for depositors, although as I said yesterday, I believe the FSCS is too generous.4 -

I don’t disagree, you buy the shares/investment and take risk of loss, against the prospect of rewards. However, in one day Lloyds was changed from one of the most solvent banks in the UK, to Lloyds/HBOS a debt laden failure. The UK Government, basically threw Lloyds under the bus, rather than nationalise HBOS. Following the crash and run on the Northern Rock Building Society, the Government could not allow another failure. This case is in my knowledge unique, and cannot be compared to issues today, with Utility companies and other public quoted entities. To this day Gordon Brown and Eric Daniels (Lloyds CEO) are hated, by Lloyds staff.golfaddick said:

I stand corrected, although as that piece says, what did the taxpayer lose in the interim with austerity & the money could have been used elsewhere.RaplhMilne said:I just like the true facts of this case to be seen. Many people believe their Tax money saved Lloyds Bank. That is completely untrue. The facts are that Lloyds Bank shareholders saved the UK Government from an unprecedented run on the banking sector not seen since the 1920,s.

I'm of the firm belief that shareholders should never be bailed out. You buy shares in the knowledge of the risk involved. Different for depositors, although as I said yesterday, I believe the FSCS is too generous.3 -

Most banks have suffered on the share price since 2008.RaplhMilne said:

I don’t disagree, you buy the shares/investment and take risk of loss, against the prospect of rewards. However, in one day Lloyds was changed from one of the most solvent banks in the UK, to Lloyds/HBOS a debt laden failure. The UK Government, basically threw Lloyds under the bus, rather than nationalise HBOS. Following the crash and run on the Northern Rock Building Society, the Government could not allow another failure. This case is in my knowledge unique, and cannot be compared to issues today, with Utility companies and other public quoted entities. To this day Gordon Brown and Eric Daniels (Lloyds CEO) are hated, by Lloyds staff.golfaddick said:

I stand corrected, although as that piece says, what did the taxpayer lose in the interim with austerity & the money could have been used elsewhere.RaplhMilne said:I just like the true facts of this case to be seen. Many people believe their Tax money saved Lloyds Bank. That is completely untrue. The facts are that Lloyds Bank shareholders saved the UK Government from an unprecedented run on the banking sector not seen since the 1920,s.

I'm of the firm belief that shareholders should never be bailed out. You buy shares in the knowledge of the risk involved. Different for depositors, although as I said yesterday, I believe the FSCS is too generous.

Natwest is one of the worst, a high wasn't it of 6500 now less than 10% of that. Barclays were around 2200, now 380.

For staff owning shares they tend to sit on them rather than trade, if they'd have traded in and out they would likely have done OK.

I get and buy shares in my company, like i've always done, I tend to sell at the earliest opportunity. As I haven't actively chosen that share I like to get out ASAP!

I've bought and sold both Barclays and Lloyds shares over the past 10 year and have done quite well on them.1 -

I'm having a look at my accounts and have two S and S ISA's - one with HL and one with Fidelity. I'd like to transfer them both to cash ISAs. How do I do this and not lose the tax benefits? Is now a good/bad time to do this?0

-

You should be able to transfer an HL S&S ISA to an HL cash ISA very easily, and then to another cash ISA provider if you want to. I'd imagine Fidelity are similar. You would not lose the tax benefits as long as you dont cash out the S&S ISAs and reinvest - just keep the funds within the ISA wrapper.Is now a good time to do it? Your guess is as good as mine. Actually better than mine as I have no idea of your circumstances, attitude to risk or your financial aims. Good luck!4

-

When you open the cash isa state on the application that you want to transfer in from a s & s isa and provide the relevant companies details and your account details on the application. The new provider contacts the existing provider and transfers the amount specified (doesn’t have to be the whole pot)

3 -

Sponsored links:

-

I went to Civil Servants "Do" when I worked for the DVSA, and partnered up with a HEO from HMRC special compliance.Er_Be_Ab_Pl_Wo_Wo_Ch said:I've been due back some tax, from my 2023/2024 self-assessment return, refund request submitted April 2024. The payment turned up today, after 19 months. HMRC must have a hefty backlog going on!

He told me that a new computer system had been stress tested and failed miserably.

That was about 3yrs ago, so it maybe not up and running.

Mind Civil Service and IT systems Updates are normally a recipe for total chaos.0 -

I had a S&S Isa with Vanguard, switched it to Trading 212 where I have both a cash and S&S ISA and it's really easy at that point to move between the two. Think they are still one of the highest paying for a cash ISA rates.Arsenetatters said:I'm having a look at my accounts and have two S and S ISA's - one with HL and one with Fidelity. I'd like to transfer them both to cash ISAs. How do I do this and not lose the tax benefits? Is now a good/bad time to do this?2 -

3.85%0

-

Good or bad time for what ? Good time to cash in gains made before stockmarkets fall ? Bad time if they surge ahead even more ? Good time to bag a good fixed interest rate on a Cash ISA before interest rates fall further?Arsenetatters said:I'm having a look at my accounts and have two S and S ISA's - one with HL and one with Fidelity. I'd like to transfer them both to cash ISAs. How do I do this and not lose the tax benefits? Is now a good/bad time to do this?

Too many questions & not enough detail.0 -

Yep the t212 stocks and shares cash interest is really good. It’s where my emergency fund is kept.Rob7Lee said:

I had a S&S Isa with Vanguard, switched it to Trading 212 where I have both a cash and S&S ISA and it's really easy at that point to move between the two. Think they are still one of the highest paying for a cash ISA rates.Arsenetatters said:I'm having a look at my accounts and have two S and S ISA's - one with HL and one with Fidelity. I'd like to transfer them both to cash ISAs. How do I do this and not lose the tax benefits? Is now a good/bad time to do this?

t212 have said they were going to offer SIPPs this year, but that remains to be seen, would be extremely interested in moving my vanguard SIPP to trading 212.0 -

Yes and being a flexible ISA you can withdraw and pay in as your hearts content!!Diebythesword said:

Yep the t212 stocks and shares cash interest is really good. It’s where my emergency fund is kept.Rob7Lee said:

I had a S&S Isa with Vanguard, switched it to Trading 212 where I have both a cash and S&S ISA and it's really easy at that point to move between the two. Think they are still one of the highest paying for a cash ISA rates.Arsenetatters said:I'm having a look at my accounts and have two S and S ISA's - one with HL and one with Fidelity. I'd like to transfer them both to cash ISAs. How do I do this and not lose the tax benefits? Is now a good/bad time to do this?

t212 have said they were going to offer SIPPs this year, but that remains to be seen, would be extremely interested in moving my vanguard SIPP to trading 212.0 -

Rob7Lee said:

Partly agree, but this is the issue with the tax free allowance being frozen yet the state pension being raised significantly (wasn't only around £7k in 2020).PragueAddick said:I may well have completely lost it, but FFS....

On what planet does it make any sense to tax a State pension, whose payments are regulated by the State? Give millions of citizens money and then make them pay back 20% or so a year later via a convuluted tax reporting system to a tax office that is barely functioning? FFS!!! If you want to reduce the size of the State pension, then do it. Reduce, or don't increase, the net payment. Not this way, by taxing it, driving everyone even more nuts with their tax returns and putting an even bigger burden on the hapless HMRC.

I mean...what am I missing here?

My solution solves all of this, make the tax free allowance £18-20k. Simples........ Anyone earning over around £125k doesn't get the allowance anyway, so it can't be said to be helping the richest. Then just tweak the 20/40 and maybe 45p bands to a slightly higher level to balance out along with in work benefits. You'd likely also raise more VAT as for the lower earners the additional net income will be spent rather than saved.

A quick search on the web reveals that there are currently around 13M pensioners in the UK with just 10% on only the state pension. In other words 90% of pensioners have occupational pensions or other income streams to see them into old age. Raising the tax free allowance is indeed a simple solution. But also incredibly expensive for the government in these times when balancing the near term budget and long term forecasts is far from easy.

A far better solution would be to automate tax return generation based upon all data available, including bank statements and leave individuals to self certify or bring in a tax expert if their affairs are more complex.

The real challenge for UK PLC is those avoiding or even evading tax by going offshore or simply under declaring earnings. It's no coincidence that those on the far right advocating a populist £20K tax free allowance live in places such as Dubai, as well as making up numbers about what might be saved by excluding immigrants from the benefits system.

We should all think very carefully about what is required from the state in terms of health, defence, schools as well as benefits and pensions. And then think about where the growth and taxable income might come from to meet the bills, plus underpin UK credibility to borrow money at decent rates.

One core question which has been kicked into the long grass is social care. Should pensioners pay NI or a property tax so as to fund this properly as well as spreading the burden? Or do we believe that everybody should take their chances with the lifestyle / DNA mix that determines how much social care might be required? Social Care patients who have no care provision established take up 1 in 6 NHS beds so it's kinda vital to address who pays and who provides asap.

At the moment social care is provided by local councils whose tax base is the out of date Council Tax based upon 1990 valustions as well as antiquated concept of business rates plus a central Gov't bursary. So please can we stop talking about tax giveaways and the supposed hardship of filling in tax returns... and instead focus upon what the country is facing, and who should pay!

From Google AI overview:Key Drivers of the 2030 Crisis- Aging Population & Long-Term Conditions:An expanding elderly population, along with more people living longer with complex, long-term health needs, dramatically increases the demand for social care services.

Chronic Underfunding:The social care system in the UK is widely considered to be chronically underfunded, with a lack of a long-term funding settlement hindering effective planning.Workforce Shortages:A significant shortage of staff is a central issue, leading to high vacancy rates and increased pressure on existing workers.Rising Costs:The cost of providing care services continues to rise, further straining budgets and contributing to the overall funding gap.2 -

I'd love to see the proposals and workings out that the volume of consultants (not medical consultants) non-doctor or nurse management come up with. Regardless of how much of a shortfall there may be, to properly fund and run the NHS. Then we could have a vote on how we proceed with that, as a country as opposed to people with one eye on re-election in a few years so want to make popular decisions as opposed to correct ones

One thing the NHS isnt short of is data, last few times I've been to the doctor I've spent more times answering data gathering questions than discussing whatever I'm there for. AI can be used legitimately to identify so much.

1 -

It's only incredibly expensive if you do nothing else, which of course as I have highlighted, would be essential to do.seriously_red said:Rob7Lee said:

Partly agree, but this is the issue with the tax free allowance being frozen yet the state pension being raised significantly (wasn't only around £7k in 2020).PragueAddick said:I may well have completely lost it, but FFS....

On what planet does it make any sense to tax a State pension, whose payments are regulated by the State? Give millions of citizens money and then make them pay back 20% or so a year later via a convuluted tax reporting system to a tax office that is barely functioning? FFS!!! If you want to reduce the size of the State pension, then do it. Reduce, or don't increase, the net payment. Not this way, by taxing it, driving everyone even more nuts with their tax returns and putting an even bigger burden on the hapless HMRC.

I mean...what am I missing here?

My solution solves all of this, make the tax free allowance £18-20k. Simples........ Anyone earning over around £125k doesn't get the allowance anyway, so it can't be said to be helping the richest. Then just tweak the 20/40 and maybe 45p bands to a slightly higher level to balance out along with in work benefits. You'd likely also raise more VAT as for the lower earners the additional net income will be spent rather than saved.

A quick search on the web reveals that there are currently around 13M pensioners in the UK with just 10% on only the state pension. In other words 90% of pensioners have occupational pensions or other income streams to see them into old age. Raising the tax free allowance is indeed a simple solution. But also incredibly expensive for the government in these times when balancing the near term budget and long term forecasts is far from easy.

You could easily balance the tax bands and other allowances/benefits so those at the bottom of the earning spectrum are a little better off.

It may need to be done in stages, move it to £15k next tax year, £17.5k the year after etc. Taxing people who earn £15k a year is just plain madness what ever the state of the public finances. Someone on £15k a year pays around £675 in tax (income & NI), if they weren't you could almost guarantee every penny of that £675 would be spent which in itself would help the economy (and you'd get some back in VAT!).

That's before we get into the fact the bands are frozen, that too is hurting the economy.3 -

The trouble is the level of governance around health data because people are shit scared and generally don't understand what happens with their data. There are rules around what data can be used for what purposes by who, what can be linked to what, compared with what. Even when its all aggregated or pseudonymised. Some legitimate protections some massively over the top. It holds back a lot of potential progress from that data.Carter said:I'd love to see the proposals and workings out that the volume of consultants (not medical consultants) non-doctor or nurse management come up with. Regardless of how much of a shortfall there may be, to properly fund and run the NHS. Then we could have a vote on how we proceed with that, as a country as opposed to people with one eye on re-election in a few years so want to make popular decisions as opposed to correct ones

One thing the NHS isnt short of is data, last few times I've been to the doctor I've spent more times answering data gathering questions than discussing whatever I'm there for. AI can be used legitimately to identify so much.0 -

Sponsored links:

-

Take 2% off NI and put it on income tax is something I can get behind.0

-

Pensioners are already falling into being taxed due to the threshold being frozen.Huskaris said:Take 2% off NI and put it on income tax is something I can get behind.

Putting 2% on the basic rate of tax will only hurt them further.

What Starmer and Reeves should do is face down the left wing back benchers and cut the enormous amount that is being wasted on welfare and various other public sectors.

They won't do this though as Starmer has no backbone and he is going to have to go back on Labour's promise not to put up taxes for the working man.2 -

One of the things they need to face up to is pensioners and the triple lock, which privately all parties know is a disaster. The tax allowance should be above the state pension, but the income tax shift should happen in my opinion.blackpool72 said:

Pensioners are already falling into being taxed due to the threshold being frozen.Huskaris said:Take 2% off NI and put it on income tax is something I can get behind.

Putting 2% on the basic rate of tax will only hurt them further.

What Starmer and Reeves should do is face down the left wing back benchers and cut the enormous amount that is being wasted on welfare and various other public sectors.

They won't do this though as Starmer has no backbone and he is going to have to go back on Labour's promise not to put up taxes for the working man.

Completely agree with you on the welfare bill, that absolutely has to be adjusted. Just taxing the same people more and more won't work.3 -

Get rid of the triple lock and go back to cutting the winter fuel allowance properly and that will make a significant dent in the black hole reeves needs to fill, whilst not taxing people to death and allowing room for some growth.The triple lock will be seen as an utter disaster, if it hasn’t already - imagine guaranteeing pay rises for benefit claimants, they’d be political uproar.25% of pensioners are millionaires, they can take the hit.3

-

Tax the rich.5

-

We’re already doing that.Friend Or Defoe said:Tax the rich.5 -

Ummm...where did you get that snippet? Very hard to believe...or have I been whooshed!Diebythesword said:Get rid of the triple lock and go back to cutting the winter fuel allowance properly and that will make a significant dent in the black hole reeves needs to fill, whilst not taxing people to death and allowing room for some growth.The triple lock will be seen as an utter disaster, if it hasn’t already - imagine guaranteeing pay rises for benefit claimants, they’d be political uproar.25% of pensioners are millionaires, they can take the hit.4 -

https://www.telegraph.co.uk/money/pensions/news/number-millionaire-pensioners-quadruples/CafcWest said:

Ummm...where did you get that snippet? Very hard to believe...or have I been whooshed!Diebythesword said:Get rid of the triple lock and go back to cutting the winter fuel allowance properly and that will make a significant dent in the black hole reeves needs to fill, whilst not taxing people to death and allowing room for some growth.The triple lock will be seen as an utter disaster, if it hasn’t already - imagine guaranteeing pay rises for benefit claimants, they’d be political uproar.25% of pensioners are millionaires, they can take the hit.

0 -

Wow...thanks but very hard to believe - can't read the full article but I suspect that property accounts for much of the wealth that makes retired people a millionaire - rising house values over a lifetime. I've always considered someone a 'proper' millionaire if they have a million in cash and liquid assets - not bricks and mortar...Diebythesword said:

https://www.telegraph.co.uk/money/pensions/news/number-millionaire-pensioners-quadruples/CafcWest said:

Ummm...where did you get that snippet? Very hard to believe...or have I been whooshed!Diebythesword said:Get rid of the triple lock and go back to cutting the winter fuel allowance properly and that will make a significant dent in the black hole reeves needs to fill, whilst not taxing people to death and allowing room for some growth.The triple lock will be seen as an utter disaster, if it hasn’t already - imagine guaranteeing pay rises for benefit claimants, they’d be political uproar.25% of pensioners are millionaires, they can take the hit.11 -

There are a lot of pensioners, living a very frugal life in the South East whilst living in a 3 bed semi worth £700- £800,000. I really don’t consider them to be rich.CafcWest said:

Wow...thanks but very hard to believe - can't read the full article but I suspect that property accounts for much of the wealth that makes retired people a millionaire - rising house values over a lifetime. I've always considered someone a 'proper' millionaire if they have a million in cash and liquid assets - not bricks and mortar...Diebythesword said:

https://www.telegraph.co.uk/money/pensions/news/number-millionaire-pensioners-quadruples/CafcWest said:

Ummm...where did you get that snippet? Very hard to believe...or have I been whooshed!Diebythesword said:Get rid of the triple lock and go back to cutting the winter fuel allowance properly and that will make a significant dent in the black hole reeves needs to fill, whilst not taxing people to death and allowing room for some growth.The triple lock will be seen as an utter disaster, if it hasn’t already - imagine guaranteeing pay rises for benefit claimants, they’d be political uproar.25% of pensioners are millionaires, they can take the hit.The problem is solved by collecting the existing taxes that are avoided, rather than additional tax on those already paying. We all have Black Cab mates, who tell you the game was screwed, when people started paying by card and cash takings dried up.It’s just easier to hit thousands of pensioners, than it is thousands of self employed Plumbers. As it is to hit UK Banks and large companies, than chase the smaller enterprises.

An I know so many people claiming £hundreds a month on PIP who pretty much have nothing wrong with them. Managed to fool a busy doctor once, and ride the gravy train forever.9