Interest rates

Comments

-

Brexit dividend/crisis1

-

Lets see, who will this help, oh yes I remember.......!3

-

I don't know yet if this is good or bad... being on a fixed term mortgage with 3.5 years remaining, I hope we miss any hitch and catch the downward trend next time!0

-

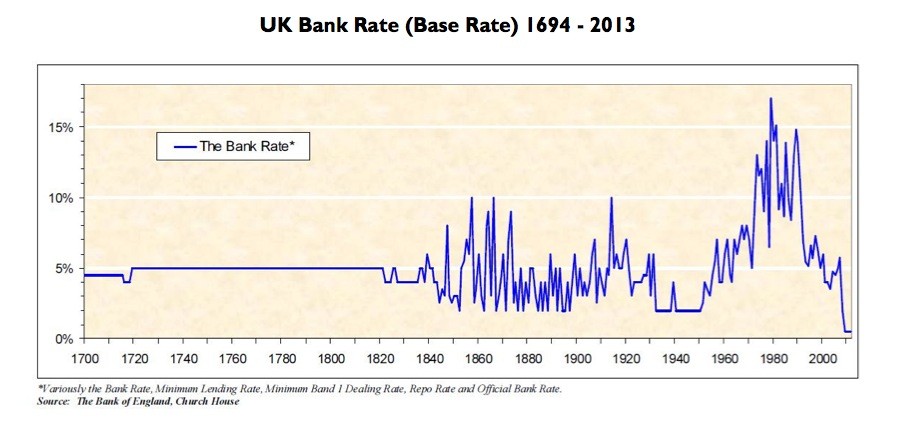

I used to be so jealous of my friends working in the banking sector who were only paying 2% interest on their mortgages.

Then we had 'Black Wednesday' when interest rates were hiked up temporarily to 15%.

0.75%? Pah…...1 -

But the size of some mortgages out there now, it wont take too much to knock some people over ...............Addickted said:I used to be so jealous of my friends working in the banking sector who were only paying 2% interest on their mortgages.

Then we had 'Black Wednesday' when interest rates were hiked up temporarily to 15%.

0.75%? Pah…...

5 -

About time too

Rates have been far too low for ages, when you look at historical rates, even during wars and economic crises 2

2 -

1720 to 1820 - what a time to be alive.25

-

Not going to make much difference. Those on trackers/variables will go up by the full amount, those with savings may see a small tick up but won't be the full 0.25%. Borrowing is still cheap as chips, I remember changing jobs to go and work for a building society to take advantage of the 5% staff mortgage! That was worth a lot back then, rates were roughly 10% so was a big saving.4

-

Happy hour.WSS said:1720 to 1820 - what a time to be alive.

14 -

"Any changes in the interest rate?"WSS said:1720 to 1820 - what a time to be alive.

"No, same again"

"Ok, see you in 10 years time"2 -

Sponsored links:

-

This has been on the cards for ages, fortunately it shouldn't hurt people Too much however it's only going to go one way0

-

Oh no doubt my mate, at least you can take your pension before me0

-

A £175k mortgage will mean about a £25pm increase. Anyone with a £500k mortgage (thus about a £70pm increase) can probably afford it.1905 said:

But the size of some mortgages out there now, it wont take too much to knock some people over ...............Addickted said:I used to be so jealous of my friends working in the banking sector who were only paying 2% interest on their mortgages.

Then we had 'Black Wednesday' when interest rates were hiked up temporarily to 15%.

0.75%? Pah…...

Next increase (again 0.25%) wont be for another year or so.....certainly at least 3 months after Brexit.

you never know, rates might even go back down again if Brexit is a total f**k up.1 -

With my millions of pounds stashed in my post office savings account this should make a heap of a difference :-|0

-

The interest rate is increased - and immediately the pound slumps.

0 -

If Brexit is a fcuk up then rates will go up not down to try to avert a currency crisisgolfaddick said:

A £175k mortgage will mean about a £25pm increase. Anyone with a £500k mortgage (thus about a £70pm increase) can probably afford it.1905 said:

But the size of some mortgages out there now, it wont take too much to knock some people over ...............Addickted said:I used to be so jealous of my friends working in the banking sector who were only paying 2% interest on their mortgages.

Then we had 'Black Wednesday' when interest rates were hiked up temporarily to 15%.

0.75%? Pah…...

Next increase (again 0.25%) wont be for another year or so.....certainly at least 3 months after Brexit.

you never know, rates might even go back down again if Brexit is a total f**k up.

0 -

I’m no expert but wasn’t the whole rate drop in line with the financial crash of 2007/08 when they needed liquidity and money pumped into the markets via QE and then encouraging everyone to borrow and banks to lend again?newyorkaddick said:

If Brexit is a fcuk up then rates will go up not down to try to avert a currency crisisgolfaddick said:

A £175k mortgage will mean about a £25pm increase. Anyone with a £500k mortgage (thus about a £70pm increase) can probably afford it.1905 said:

But the size of some mortgages out there now, it wont take too much to knock some people over ...............Addickted said:I used to be so jealous of my friends working in the banking sector who were only paying 2% interest on their mortgages.

Then we had 'Black Wednesday' when interest rates were hiked up temporarily to 15%.

0.75%? Pah…...

Next increase (again 0.25%) wont be for another year or so.....certainly at least 3 months after Brexit.

you never know, rates might even go back down again if Brexit is a total f**k up.

Presumably it’s been too low for too long now?

1 -

Yes, 10 years is ridiculous and distorts the economy, and probably has kept house prices artificially high toocabbles said:

I’m no expert but wasn’t the whole rate drop in line with the financial crash of 2007/08 when they needed liquidity and money pumped into the markets via QE and then encouraging everyone to borrow and banks to lend again?newyorkaddick said:

If Brexit is a fcuk up then rates will go up not down to try to avert a currency crisisgolfaddick said:

A £175k mortgage will mean about a £25pm increase. Anyone with a £500k mortgage (thus about a £70pm increase) can probably afford it.1905 said:

But the size of some mortgages out there now, it wont take too much to knock some people over ...............Addickted said:I used to be so jealous of my friends working in the banking sector who were only paying 2% interest on their mortgages.

Then we had 'Black Wednesday' when interest rates were hiked up temporarily to 15%.

0.75%? Pah…...

Next increase (again 0.25%) wont be for another year or so.....certainly at least 3 months after Brexit.

you never know, rates might even go back down again if Brexit is a total f**k up.

Presumably it’s been too low for too long now?1 -

Sponsored links:

-

The financial crisis was a global phenomenon but a hard Brexit would be our problem alonecabbles said:

I’m no expert but wasn’t the whole rate drop in line with the financial crash of 2007/08 when they needed liquidity and money pumped into the markets via QE and then encouraging everyone to borrow and banks to lend again?newyorkaddick said:

If Brexit is a fcuk up then rates will go up not down to try to avert a currency crisisgolfaddick said:

A £175k mortgage will mean about a £25pm increase. Anyone with a £500k mortgage (thus about a £70pm increase) can probably afford it.1905 said:

But the size of some mortgages out there now, it wont take too much to knock some people over ...............Addickted said:I used to be so jealous of my friends working in the banking sector who were only paying 2% interest on their mortgages.

Then we had 'Black Wednesday' when interest rates were hiked up temporarily to 15%.

0.75%? Pah…...

Next increase (again 0.25%) wont be for another year or so.....certainly at least 3 months after Brexit.

you never know, rates might even go back down again if Brexit is a total f**k up.

Presumably it’s been too low for too long now?

1 -

And I’m assuming rates can’t go up too high because of the amount of debt swilling around now? We’re sort of stuck on what are likely to be lower rates for a very long time???killerandflash said:

Yes, 10 years is ridiculous and distorts the economy, and probably has kept house prices artificially high toocabbles said:

I’m no expert but wasn’t the whole rate drop in line with the financial crash of 2007/08 when they needed liquidity and money pumped into the markets via QE and then encouraging everyone to borrow and banks to lend again?newyorkaddick said:

If Brexit is a fcuk up then rates will go up not down to try to avert a currency crisisgolfaddick said:

A £175k mortgage will mean about a £25pm increase. Anyone with a £500k mortgage (thus about a £70pm increase) can probably afford it.1905 said:

But the size of some mortgages out there now, it wont take too much to knock some people over ...............Addickted said:I used to be so jealous of my friends working in the banking sector who were only paying 2% interest on their mortgages.

Then we had 'Black Wednesday' when interest rates were hiked up temporarily to 15%.

0.75%? Pah…...

Next increase (again 0.25%) wont be for another year or so.....certainly at least 3 months after Brexit.

you never know, rates might even go back down again if Brexit is a total f**k up.

Presumably it’s been too low for too long now?

0 -

Carney said they could rise to 2% to 3% over the medium to long term, but not 5% which is the more historical average.cabbles said:

And I’m assuming rates can’t go up too high because of the amount of debt swilling around now? We’re sort of stuck on what are likely to be lower rates for a very long time???killerandflash said:

Yes, 10 years is ridiculous and distorts the economy, and probably has kept house prices artificially high toocabbles said:

I’m no expert but wasn’t the whole rate drop in line with the financial crash of 2007/08 when they needed liquidity and money pumped into the markets via QE and then encouraging everyone to borrow and banks to lend again?newyorkaddick said:

If Brexit is a fcuk up then rates will go up not down to try to avert a currency crisisgolfaddick said:

A £175k mortgage will mean about a £25pm increase. Anyone with a £500k mortgage (thus about a £70pm increase) can probably afford it.1905 said:

But the size of some mortgages out there now, it wont take too much to knock some people over ...............Addickted said:I used to be so jealous of my friends working in the banking sector who were only paying 2% interest on their mortgages.

Then we had 'Black Wednesday' when interest rates were hiked up temporarily to 15%.

0.75%? Pah…...

Next increase (again 0.25%) wont be for another year or so.....certainly at least 3 months after Brexit.

you never know, rates might even go back down again if Brexit is a total f**k up.

Presumably it’s been too low for too long now?0 -

In a crisis rates will go where markets dictate they go not where the BoE would like them to go - see 1992 for a historical precedent.Covered End said:

Carney said they could rise to 2% to 3% over the medium to long term, but not 5% which is the more historical average.cabbles said:

And I’m assuming rates can’t go up too high because of the amount of debt swilling around now? We’re sort of stuck on what are likely to be lower rates for a very long time???killerandflash said:

Yes, 10 years is ridiculous and distorts the economy, and probably has kept house prices artificially high toocabbles said:

I’m no expert but wasn’t the whole rate drop in line with the financial crash of 2007/08 when they needed liquidity and money pumped into the markets via QE and then encouraging everyone to borrow and banks to lend again?newyorkaddick said:

If Brexit is a fcuk up then rates will go up not down to try to avert a currency crisisgolfaddick said:

A £175k mortgage will mean about a £25pm increase. Anyone with a £500k mortgage (thus about a £70pm increase) can probably afford it.1905 said:

But the size of some mortgages out there now, it wont take too much to knock some people over ...............Addickted said:I used to be so jealous of my friends working in the banking sector who were only paying 2% interest on their mortgages.

Then we had 'Black Wednesday' when interest rates were hiked up temporarily to 15%.

0.75%? Pah…...

Next increase (again 0.25%) wont be for another year or so.....certainly at least 3 months after Brexit.

you never know, rates might even go back down again if Brexit is a total f**k up.

Presumably it’s been too low for too long now?1 -

Obviously.newyorkaddick said:

In a crisis rates will go where markets dictate they go not where the BoE would like them to go - see 1992 for a historical precedent.Covered End said:

Carney said they could rise to 2% to 3% over the medium to long term, but not 5% which is the more historical average.cabbles said:

And I’m assuming rates can’t go up too high because of the amount of debt swilling around now? We’re sort of stuck on what are likely to be lower rates for a very long time???killerandflash said:

Yes, 10 years is ridiculous and distorts the economy, and probably has kept house prices artificially high toocabbles said:

I’m no expert but wasn’t the whole rate drop in line with the financial crash of 2007/08 when they needed liquidity and money pumped into the markets via QE and then encouraging everyone to borrow and banks to lend again?newyorkaddick said:

If Brexit is a fcuk up then rates will go up not down to try to avert a currency crisisgolfaddick said:

A £175k mortgage will mean about a £25pm increase. Anyone with a £500k mortgage (thus about a £70pm increase) can probably afford it.1905 said:

But the size of some mortgages out there now, it wont take too much to knock some people over ...............Addickted said:I used to be so jealous of my friends working in the banking sector who were only paying 2% interest on their mortgages.

Then we had 'Black Wednesday' when interest rates were hiked up temporarily to 15%.

0.75%? Pah…...

Next increase (again 0.25%) wont be for another year or so.....certainly at least 3 months after Brexit.

you never know, rates might even go back down again if Brexit is a total f**k up.

Presumably it’s been too low for too long now?0 -

The B of E is increasing rates with the intention of transferring money in our pockets away from spending on goods and services and to inhibit the growth of new debt by making it more expensive. Protecting us from the impact of variable mortgage, a commercial risk taken on by us voluntarily, is a political objective rather than an economic one. The B of E is in theory immune from political pressures and acts in the interests of the wider economy.cabbles said:

And I’m assuming rates can’t go up too high because of the amount of debt swilling around now? We’re sort of stuck on what are likely to be lower rates for a very long time???killerandflash said:

Yes, 10 years is ridiculous and distorts the economy, and probably has kept house prices artificially high toocabbles said:

I’m no expert but wasn’t the whole rate drop in line with the financial crash of 2007/08 when they needed liquidity and money pumped into the markets via QE and then encouraging everyone to borrow and banks to lend again?newyorkaddick said:

If Brexit is a fcuk up then rates will go up not down to try to avert a currency crisisgolfaddick said:

A £175k mortgage will mean about a £25pm increase. Anyone with a £500k mortgage (thus about a £70pm increase) can probably afford it.1905 said:

But the size of some mortgages out there now, it wont take too much to knock some people over ...............Addickted said:I used to be so jealous of my friends working in the banking sector who were only paying 2% interest on their mortgages.

Then we had 'Black Wednesday' when interest rates were hiked up temporarily to 15%.

0.75%? Pah…...

Next increase (again 0.25%) wont be for another year or so.....certainly at least 3 months after Brexit.

you never know, rates might even go back down again if Brexit is a total f**k up.

Presumably it’s been too low for too long now?

The current interest rates are being subsidised by money, in effect, given to us by the B of E. As that subsidy is gradually lifted interest rates will revert back to bearing a relationship with the real world where there is a margin to recognise the reward where money is lent in the market at a higher risk, to generate economic activity. Currently, merchant banks can lend for a margin above the near zero subsidised rate and get a handsome yield without taking much risk. Most of that money is being lent for speculation on buying and selling real assets and stocks and shares, property but little infrastructure and entrepreneurial ventures. Little of it gets to entrepreneurs because the risk is not worth taking, where the lender is currently getting the same yield for low risk loans to asset speculators, as historically the lenders got from high risk commercial ventures.

Speculators being able to buy assets for speculation with cheap money has driven up the price of all assets, including our homes.

So no one should be surprised when interests rates rise and asset prices, including our homes, fall, and our debt is not covered by the equity, when the bubble busts. It's the long term price for avoiding a short term economic disaster after the crash. The price was expected to be paid out of an increasing GDP and rising wages, but that hasn't happened because of low productivity. The danger is that the current mortgage rates are regarded as normal, unless you regard a stagnant economy with little money made available for real investment in growth as normal.

The drop in sterling reflects the market's view that the economy is not strong enough to absorb the impact on reduced spending and it could lead to recession.

2 -

thanks dip, informative as always.Dippenhall said:

The B of E is increasing rates with the intention of transferring money in our pockets away from spending on goods and services and to inhibit the growth of new debt by making it more expensive. Protecting us from the impact of variable mortgage, a commercial risk taken on by us voluntarily, is a political objective rather than an economic one. The B of E is in theory immune from political pressures and acts in the interests of the wider economy.cabbles said:

And I’m assuming rates can’t go up too high because of the amount of debt swilling around now? We’re sort of stuck on what are likely to be lower rates for a very long time???killerandflash said:

Yes, 10 years is ridiculous and distorts the economy, and probably has kept house prices artificially high toocabbles said:

I’m no expert but wasn’t the whole rate drop in line with the financial crash of 2007/08 when they needed liquidity and money pumped into the markets via QE and then encouraging everyone to borrow and banks to lend again?newyorkaddick said:

If Brexit is a fcuk up then rates will go up not down to try to avert a currency crisisgolfaddick said:

A £175k mortgage will mean about a £25pm increase. Anyone with a £500k mortgage (thus about a £70pm increase) can probably afford it.1905 said:

But the size of some mortgages out there now, it wont take too much to knock some people over ...............Addickted said:I used to be so jealous of my friends working in the banking sector who were only paying 2% interest on their mortgages.

Then we had 'Black Wednesday' when interest rates were hiked up temporarily to 15%.

0.75%? Pah…...

Next increase (again 0.25%) wont be for another year or so.....certainly at least 3 months after Brexit.

you never know, rates might even go back down again if Brexit is a total f**k up.

Presumably it’s been too low for too long now?

The current interest rates are being subsidised by money, in effect, given to us by the B of E. As that subsidy is gradually lifted interest rates will revert back to bearing a relationship with the real world where there is a margin to recognise the reward where money is lent in the market at a higher risk, to generate economic activity. Currently, merchant banks can lend for a margin above the near zero subsidised rate and get a handsome yield without taking much risk. Most of that money is being lent for speculation on buying and selling real assets and stocks and shares, property but little infrastructure and entrepreneurial ventures. Little of it gets to entrepreneurs because the risk is not worth taking, where the lender is currently getting the same yield for low risk loans to asset speculators, as historically the lenders got from high risk commercial ventures.

Speculators being able to buy assets for speculation with cheap money has driven up the price of all assets, including our homes.

So no one should be surprised when interests rates rise and asset prices, including our homes, fall, and our debt is not covered by the equity, when the bubble busts. It's the long term price for avoiding a short term economic disaster after the crash. The price was expected to be paid out of an increasing GDP and rising wages, but that hasn't happened because of low productivity. The danger is that the current mortgage rates are regarded as normal, unless you regard a stagnant economy with little money made available for real investment in growth as normal.

The drop in sterling reflects the market's view that the economy is not strong enough to absorb the impact on reduced spending and it could lead to recession.

without knowing much about macro or micro economics I've been feeling for some time that we're heading for a bit of a shock0 -

I Remember the days when the rate went up a few times in a single day and were around 15%. .75% is nothing.0

-

The level of debt is very worrying - this has been ongoing since the 1990s and successive governments have done nothing to address this. Asset prices as you say are due for a correction but it seems unlikely that this will be managed.Dippenhall said:

The B of E is increasing rates with the intention of transferring money in our pockets away from spending on goods and services and to inhibit the growth of new debt by making it more expensive. Protecting us from the impact of variable mortgage, a commercial risk taken on by us voluntarily, is a political objective rather than an economic one. The B of E is in theory immune from political pressures and acts in the interests of the wider economy.cabbles said:

And I’m assuming rates can’t go up too high because of the amount of debt swilling around now? We’re sort of stuck on what are likely to be lower rates for a very long time???killerandflash said:

Yes, 10 years is ridiculous and distorts the economy, and probably has kept house prices artificially high toocabbles said:

I’m no expert but wasn’t the whole rate drop in line with the financial crash of 2007/08 when they needed liquidity and money pumped into the markets via QE and then encouraging everyone to borrow and banks to lend again?newyorkaddick said:

If Brexit is a fcuk up then rates will go up not down to try to avert a currency crisisgolfaddick said:

A £175k mortgage will mean about a £25pm increase. Anyone with a £500k mortgage (thus about a £70pm increase) can probably afford it.1905 said:

But the size of some mortgages out there now, it wont take too much to knock some people over ...............Addickted said:I used to be so jealous of my friends working in the banking sector who were only paying 2% interest on their mortgages.

Then we had 'Black Wednesday' when interest rates were hiked up temporarily to 15%.

0.75%? Pah…...

Next increase (again 0.25%) wont be for another year or so.....certainly at least 3 months after Brexit.

you never know, rates might even go back down again if Brexit is a total f**k up.

Presumably it’s been too low for too long now?

The current interest rates are being subsidised by money, in effect, given to us by the B of E. As that subsidy is gradually lifted interest rates will revert back to bearing a relationship with the real world where there is a margin to recognise the reward where money is lent in the market at a higher risk, to generate economic activity. Currently, merchant banks can lend for a margin above the near zero subsidised rate and get a handsome yield without taking much risk. Most of that money is being lent for speculation on buying and selling real assets and stocks and shares, property but little infrastructure and entrepreneurial ventures. Little of it gets to entrepreneurs because the risk is not worth taking, where the lender is currently getting the same yield for low risk loans to asset speculators, as historically the lenders got from high risk commercial ventures.

Speculators being able to buy assets for speculation with cheap money has driven up the price of all assets, including our homes.

So no one should be surprised when interests rates rise and asset prices, including our homes, fall, and our debt is not covered by the equity, when the bubble busts. It's the long term price for avoiding a short term economic disaster after the crash. The price was expected to be paid out of an increasing GDP and rising wages, but that hasn't happened because of low productivity. The danger is that the current mortgage rates are regarded as normal, unless you regard a stagnant economy with little money made available for real investment in growth as normal.

The drop in sterling reflects the market's view that the economy is not strong enough to absorb the impact on reduced spending and it could lead to recession.

Lenders have been reckless and the lack of credit control has been used to keep the economy afloat.0 -

The world economy was on its way to a true reckoning back in 2008-09, but a wave of free money and government spending stalled it 1/2 way through its downward spiral. It just pushed off the inevitable.

Now that we are no longer printing "free" money (where the interest charged is lower than inflation,) just this slight change alone is already starting to worry the markets. In the USA we have 3.8% unemployment, 2% inflation, a record stock market... and yet our deficit in Obama's last year was $666 billion, 50% higher than the year before. This year it will be a trillion. And this is while the economy is roaring (GDP up 4.2% last quarter here.)

God knows what happens in the next recession. But we have kicked the can down the road as far as it will go. When the music stops, and people stop spending on things like iPhones and new cars and buying houses, it will be a real mess. My wine sells for $175 per bottle. Although I am doing well right now, no one needs that when people are in fear of their next paycheck.1